This edition of Sightlines Premium, a paid subscription service for industry decision-makers, is being made available for free during the COVID-19 crisis in order to maximize the effective reach of this critical information. To sign up, join here

With over a month of data now showing how Americans have shopped during the COVID-19 pandemic, the idea of pantry-maintenance has taken hold. But while portions of the country wait to reach their peak of confirmed cases, the ebb-and-flow of beer buying is starting to hint at how restocking is taking place.

The results are similar to how states handle the crisis itself—in the lead-up to jumps of COVID-19, buying habits follow. And where a curve is successfully flattened or is yet to reach a discernible peak, sales are a bit more restrained, and spread out over time.

Previous weeks featured Fourth of July sales figures (including $816 million of beer only March 15-22) and despite an expected slowdown of purchases nationally, individual examples of states that have already hit an expected peak of COVID-19 foreshadow what may be coming for retail outlets in places still waiting to get to an apex.

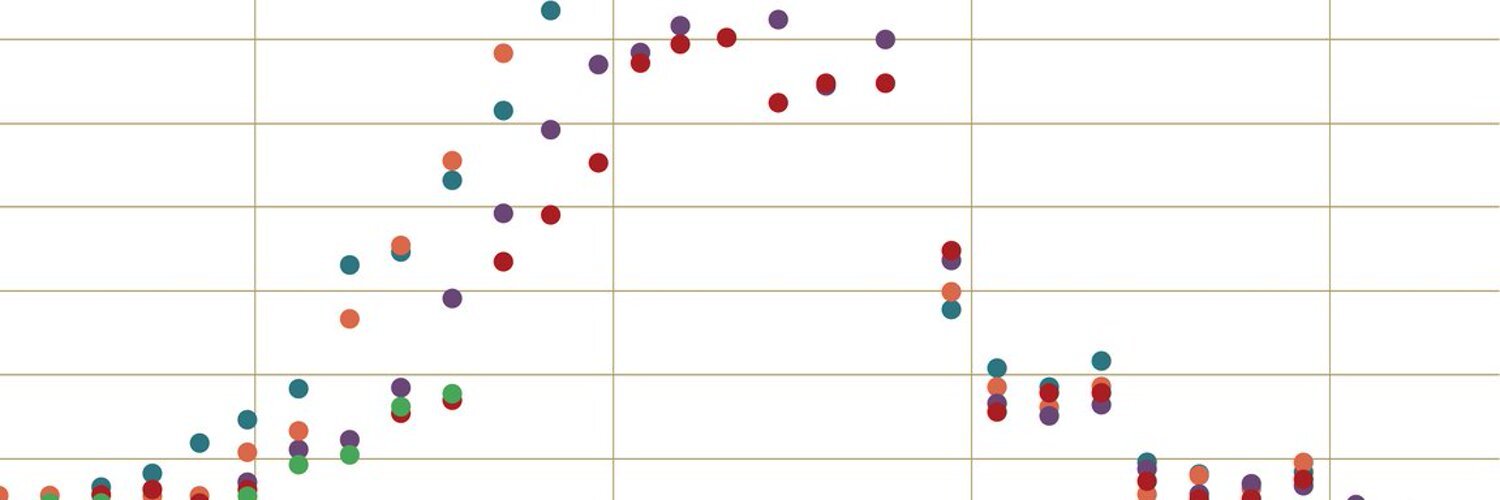

Using models created by the University of Washington and reported by NPR, Illinois is assumed to have reached its peak April 8. And in the week leading up to that, alcohol sales saw a significant jump, with IRI-tracked beer sales (including FMBs and non-alcoholic) in grocery, Walmart, and other chain stores increasing almost 26% from the week before. This came after Chicago Mayor Lori Lightfoot told the Chicago Tribune March 27 about an expected peak “sometime in April” and then an April 3 story in the newspaper looking at when the state would have its peak.

Click to enlarge

It’s impossible to directly correlate increased alcohol sales with these warnings, but using these stories as reference points can offer the closest idea of how public decision making could be taking place. Illinois saw a drop-off of about 300,000 beer case equivalents between the third and fourth week of March—presumably due to change in at-home levels of stock—then regained 126,000 CEs the following week after several days of state-wide reporting regarding the upcoming peak.

A similar pattern emerged in Michigan (April 7) and Louisiana (April 8). New York has been the epicenter of U.S. COVID-19 cases, and leading into its expected peak of April 9, saw IRI-tracked beer sales grow 10%.

Click to enlarge

Playing out with more certainty in coming weeks, the theory is this: When the public learns more information about a peak, or that peak is extended or changed, an attitude to restock will prompt additional buying. There should be an expectation of a series of smaller spikes coming state-by-state as the COVID-19 crisis goes on longer. Something as simple as monitoring local media and in-state medical response to cases could offer insight on when to expect shortened runs on groceries and alcohol. Updated charts like those from NPR are a good resource

And what about states that are yet to experience their peak? Examples like Texas (April 28) and Utah (April 29) are showing a plateau of purchases at IRI’s tracked grocery stores, and the Lone Star State was actually below national averages for beer sales the week ending April 5 compared to 2019.

This makes a place like Texas of particular interest, as it could be something of a proving ground for what we could see elsewhere. It’s a beer-loving state (#2 market in the country) and will be late to a COVID-19 peak. Beer sales have increased versus 2019, but have been tracking below the average national growth rate since March, perhaps waiting to spike later this month.

Click to enlarge

One outlier in Texas: FMBs have actually slightly declined the last three weeks of data, an aberration in the era of hard seltzer while the states mentioned above have either seen increases in FMB sales or bounce backs from the end of March's wild buying to the start of April. New Belgium, Karbach, and Real Ale have stayed strong week-to-week for IRI-defined "craft" in Texas, and Tecate made one of the biggest CE jumps from the last week of March to the first week of April.

This presents a wait-and-see scenario: Off-premise purchases have jumped everywhere, but for states that haven’t yet experienced a COVID-19 peak (or won’t have something as drastic as New York or Michigan) may just have a purchasing curve that stays higher than normal. So far, these locations have been buying in-line with national stock-up trends, but if and when lives start to get truly affected by spikes in COVID-19 cases, these curves could swing up or down.

As this plays out, it’s also worth looking toward places where COVID-19 has lasted the longest. Washington was the first state with a confirmed case on Jan. 21, but wasn’t expected to hit its high of cases until April 6. In-state sales of beer have followed national trends, hitting peaks in mid-March, but also rebounded strongly at the same time local media was covering the potential length of the pandemic and major companies like Boeing were finally suspending operations toward the end of March. Leading into its peak week, beer sales in Washington increased by about 20,000 CEs, 4.5% from the week before. Half of that growth came from craft and import brands.

Washington is a bit of an outlier due to its history of a progressive beer culture and a higher-than-average household income, but the growth of higher-priced craft and import brands connects to one expectation IRI shared in a recent market report: that as the economy struggles and stay-at-home orders are more easily accepted, middle- and upper-income households will purchase more premium products as a reward.

This is not to signal the end of runs on large package sizes—which IRI also expects to continue—but that just like how states are individually responding to the crisis and buying habits differ from place-to-place, residents’ past behavior may show some resiliency.

This article is part of the Sightlines Premium channel. Only subscribers have access to the rest of this content and community discussion.

An insights-driven professional community and content subscription for the craft beverage industry.

Introducing a premium content subscription with weekly articles, insights, and data that stimulate an ongoing conversation for brewers and beverage producers in emerging categories. Led by Michael Kiser and Bryan Roth of Good Beer Hunting, and a team of category experts, the goal is turn curiosity into actionable insights for business leaders and decision-makers.

Membership benefits:

Weekly newsletter content via

Community access

2-way dialog with GBH team

50% company discount

Words by Bryan Roth

Words by Bryan Roth