Craft beer has long held the throne for beer lovers when it comes to embodying the antithesis of Bud, Miller, and Coors. Sitting in that throne, of course, is IPA, the darling of American contrariness to Adjunct Lager. Brewers Association members don’t yet eclipse 13% of U.S. market share, but punch well above their weight in terms of societal and cultural influence, especially among craft’s biggest supporters, which are disproportionately white males.

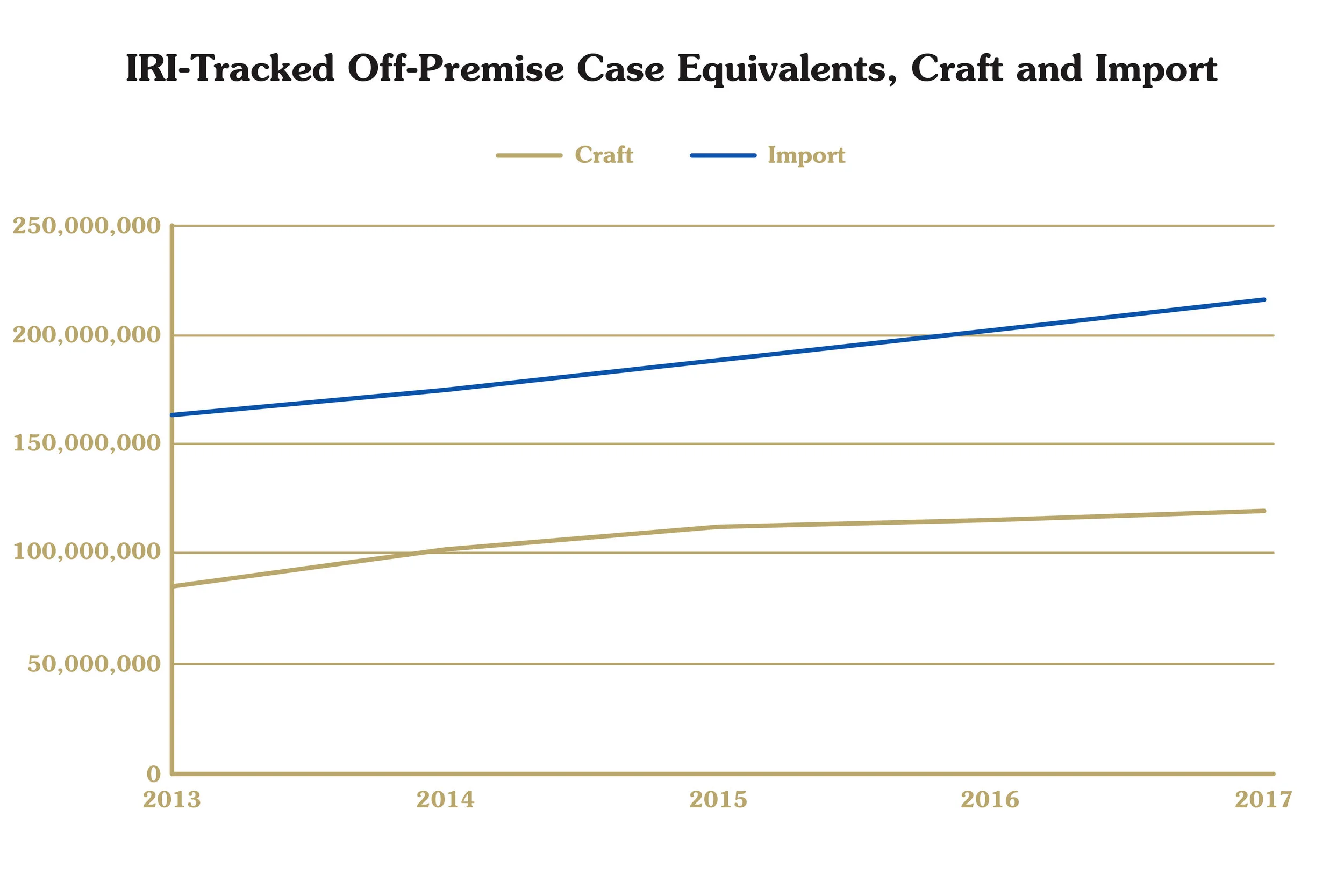

But aside from a few key brands, imports don’t present nearly the level of perceived excitement. The reality, at least when it comes to sales, is quite different. In 2017, imports to the U.S. sold about 10 million more barrels than Brewers Association-defined craft brewers. From 2014-2017, they sold an average of almost 34% more beer than craft nationwide.

All of which is a quantitatively-focused way of asking, “Why should people care about imports?”

Many drinkers’ first impression of imports might rightfully go straight to Corona Extra or Modelo Especial, easily the top-two selling imports in America, both of which sell a couple million cases more of beer in grocery, convenience, and other stores than a major macro brand like Busch Light. Heineken, #3 with a bullet, outsells Sierra Nevada, Samuel Adams, and New Belgium combined in those locations. In IRI-tracked stores, imports have considerably grown sales compared to IRI-defined craft beer, selling 72%, 69%, 75%, and 79% more volume from 2014-2017. Through mid-August, imports outsold craft by 86%.

One brand driving some of that growth is a new beer with a familiar name. Corona Premier, Constellation Brands’ answer to Michelob Ultra, was the brewery’s first new beer in almost three decades. The 90-calorie, 2.6-gram carbohydrate beer sold 2.9 million case equivalents in grocery, convenience, and other stores through mid-August—nearly the same amount as the entire Lagunitas portfolio of brands.

Stella Artois has also been a slow-growing success for Anheuser-Busch InBev, increasing its IRI sales numbers by 30% from 2015-2017 and selling more packaged product in the U.S. than the Blue Moon family of beers in 2018. Bottles sold in stores represent about 20% of the entire import volume from Belgium.

Click to enlarge

Among the more unexpected success stories is that of Peroni Nastro Azzurro, which MillerCoors recently identified as the “fastest-growing of the top 10 European import brands” according to Nielsen figures. It’s a specific title (imported European brands sold only in tracked off-premise stores), but also not one to be ignored. With about 324,000 case equivalents sold through mid-August, the Italian Pale Lager sold as much as Stone IPA and the entire 21st Amendment portfolio in stores. Given recent business trouble for MillerCoors, it’s surely a welcome surprise in 2018.

Per its company blog, “Peroni is a key entry for MillerCoors in the above-premium space, the hottest segment in beer.” In 2017, "high-end craft"—brands that cost $40 or more a case—represented just 27% of craft dollar sales, but 76% of growth, according to Bump Williams Consulting. Last year, the $40-$60 tier of case price was the fastest growing in craft.

The combination of these factors that could support an increased presence for Italian, upscale beer is what led Birra Antoniana, a six-year-old Italian brewery, to enter the U.S. market last year. The company wanted to seize on a lack of native Italian beer presence in corresponding restaurants

“It starts from the fact that when you talk about food and Italy, the very first thing that comes to everybody’s mind is pizza,” Stefania Contin, export manager for Birra Antoniana, told GBH at the time. “What we are aiming at is to pair our quality beer to great quality pizza and create a full Italian experience for the consumer.”

The company behind Peroni is looking to spin that sentiment with record-level investments in advertising. MillerCoors will push deeper into a growing collection of “prestige accounts,” which Scott Bussen, Tenth and Blake’s director of marketing communications and meetings and events, referred to as “hip, trendy accounts” in locations that draw people “who fit with the Peroni brand purpose.” He couldn’t elaborate on that description, though, since interpretation is left to localized teams.

MillerCoors had previously identified New York City, Los Angeles, and Miami as its original priority markets, but that group has since expanded to 17 locations, now including places like Las Vegas, Atlanta, and Tampa. Sales and brand ambassador teams created specifically to support Pernoi will lead the way in these markets.

Click to enlarge

Stories like Peroni, Stella Artois, or Pilsner Urquell (7.5% IRI volume growth from 2015-2017) are all great, but it’s Mexican beer that really drives the import market. In the first six months of 2018, Mexican beer sold more than six times as much volume in the U.S. than #2 country, the Netherlands. According to figures tracked by the Beer Institute, Mexico accounted for about 70% of all imported beer to the U.S. in that timeframe.

Many of these beers are marketed to and drank by drinkers of Hispanic descent, with Hispanics of Mexican origin counting for about two-thirds of the Hispanic population in the U.S. The connection between the two is not lost, as a correlation between increasing import sales and the rising non-white U.S. population are often cited together. Hispanics account for almost 20% of the U.S. population, and that number is expected to continually grow.

To show just how much of an impact Mexican beer can have, Sierra Nevada COO Joe Whitney recently said that Modelo will soon be the best-selling beer in California, producing bigger sales numbers than Bud Light, easily the #1 beer in the country. According to Brewbound, he went even further, noting that the beer would soon overtake all others in Texas, too. The U.S. Census Bureau estimates that both states have about 40% of residents who identify as Hispanic or Latino.

For as much excitement that beer enthusiasts may get from the Old World techniques of Belgium or the UK, the hold Mexican beer has on the U.S. import market is not likely to ever loosen. Recent years have even seen American craft brewers play in this space, looking to capitalize on an ongoing trend while appealing to a variety of new drinkers. In a smart move that reflects more attention to the diverse collection of beer drinkers, some have even managed to do so without appropriating culture in poor taste.

But like an argument the Brewers Association’s “small and independent” companies have made for their approach to craft beer, it can be hard to beat the “real thing.” Fuller-flavored products, including intent, packaging, and country of origin, all play into the consistent success of imports.

Hazy IPAs and Pastry Stouts may get the most attention on message boards, but in grocery and convenience stores, flagships from foreign countries are still selling at high volumes with no sign of letting up. While they may not be the kind of stuff obsessives would trade for online, they’re still proudly waving their flags—and with good reason.

—Bryan Roth